1

Europe racks up a record $113bn of bond sales in a single week in January, as government and corporate issuers race to get ahead of building rate hike expectations.

Europe racks up a record $113bn of bond sales in a single week in January, as government and corporate issuers race to get ahead of building rate hike expectations.

US leveraged loan funds take in $1.84bn of cash in the week ended January 12, their biggest weekly inflow since 2013, as demand for floating rate assets rises. In the same week, fixed rate US high yield bond funds see $2.2bn of outflows.

Russia invades Ukraine on February 24, a move that sends the price of key commodities soaring, with oil hitting $130 a barrel and wheat prices up 40% by early March. By October, 7.5 million Ukrainian refugees will have left the country.

In a February report S&P Global predicts global issuance of sustainable bonds will grow to $1.5tr in 2022 even as overall bond issuance stagnates. That would mean sustainable bonds accounting for 17% of total issuance, up from 11% in 2021 and 7% in 2020.

The Fed raises interest rates by 25bp at its March meeting, its first hike since 2018, as chair Jerome Powell says he is “acutely aware” of the need to control inflation. The Fed also revises its dot plots to suggest a further 150bp of hikes by the end of the year, a sharp change in guidance that will ultimately prove too conservative.

The two-year US Treasury yield surges from 1.35% to 2.35% over the course of March, as investors digest Fed guidance for more aggressive rate rises and the building inflationary impact of the war in Ukraine.

The broad fixed income sell-off sees euro investment grade bond yields quadruple in the first four months of 2022, hitting 2.1% at the end of April to exceed the peak they reached in March 2020 at the height of the COVID-19 crisis.

Emerging market debt sales see their slowest April for 10 years, as the war in Ukraine and rising interest rates deter borrowers. EM issuance in dollars and euros for April 2022 totals $30.6bn, a 48% decline on the same month a year earlier.

Global high yield bond issuance is running at its slowest pace in 13 years in May, with lower rated companies hesitant to borrow amid higher rates and spreads. Volume stands at $90bn year-to-date through May 23, barely 30% of the total for the same period in 2021.

On June 1, the Fed stops reinvesting the proceeds on up to $47.5bn of its bond holdings per month, ending an unprecedented era of expansion that has seen its balance sheet swell to almost $9 trillion. The Fed goes on to double its pace of ‘quantitative tightening’ to $95bn per month from September 1.

June is the busiest month of the year so far for green bonds, according to the Climate Bonds Initiative, with $47bn of supply helping total Q2 issuance to $121.3bn. For the second consecutive quarter, China is the most prolific country by volume ($48.2bn), number of deals (190) and number of issuers (116).

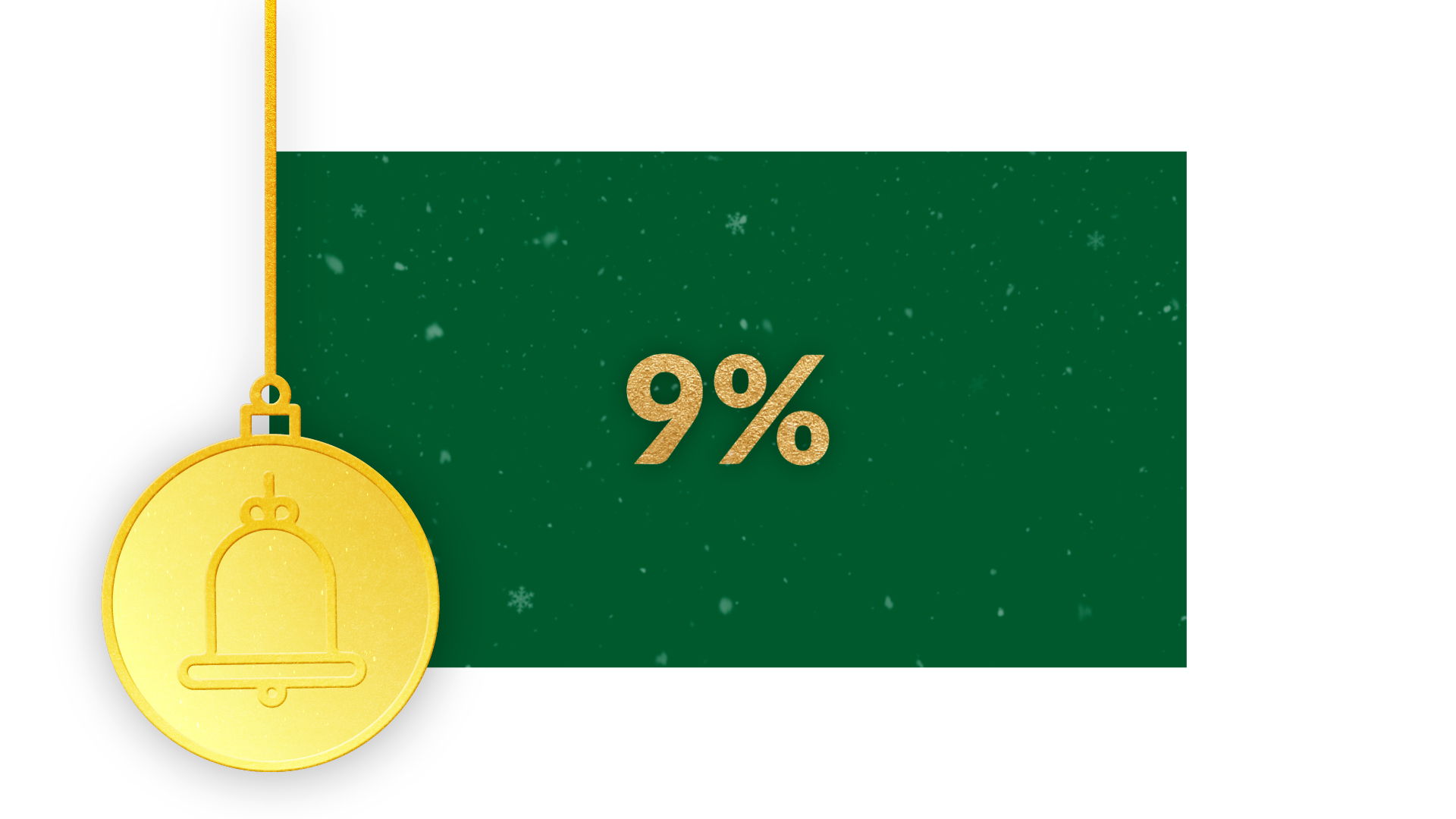

The US dollar rises 9% against a basket of major world currencies in the first half of 2022, driven by Fed rate hikes and relative US economic strength. The Japanese yen is down -15.5%.

A typical 60/40 portfolio of US stocks and bonds is down 14.8% through July 8 as the breakdown of traditional correlations leaves investors with few places to hide. By September losses are close to 20%, on course for the popular strategy’s worst year since the Great Depression.

Gas prices in Europe hit a record high of €343 per kilowatt hour in August as fears grow that Russia will cut off supply to the continent. The following month, Russia shuts down the Nord Stream 1 and 2 pipelines after they are damaged by explosions.

The Bank of England hikes interest rates by 50bp at its August meeting, its biggest increase in 27 years, but the move is overshadowed by a bearish projection for the UK economy that includes a five-quarter recession and inflation peaking at 13.2% in Q4.

By September 20 some 88% of the US investment grade corporate bond market is trading below par, as lower spread fixed rate bonds continue to suffer from central banks’ battle with inflation. Twelve months earlier, just 4% of the market was trading at a discount.

UK government bonds see some of the most volatile trading on record in late September after new finance minister Kwasi Kwarteng’s mini-Budget. Five-year Gilt yields spike by more than 50bp on September 23 alone and hit a high of almost 4.8% before the Bank of England is forced to intervene.

The cost of insuring against a Credit Suisse debt default via five-year credit default swaps soars to 355bp on October 3, after an ABC business reporter tweets that a “credible source” has told him a major international investment bank is “on the brink”. In a show of strength, the bank offers to buy back $3bn of its bonds on October 7 before announcing a sweeping restructuring later in the month.

10-year US Treasuries fall in price for 11 consecutive weeks up to mid-October, their longest losing streak since at least 1978 according to JP Morgan, as inflation and rate expectations keep relentless upward pressure on government bond yields.

US 30-year mortgage rates hit 7% in October, their highest level since 2001, as markets begin to price in a US terminal rate of more than 5%.

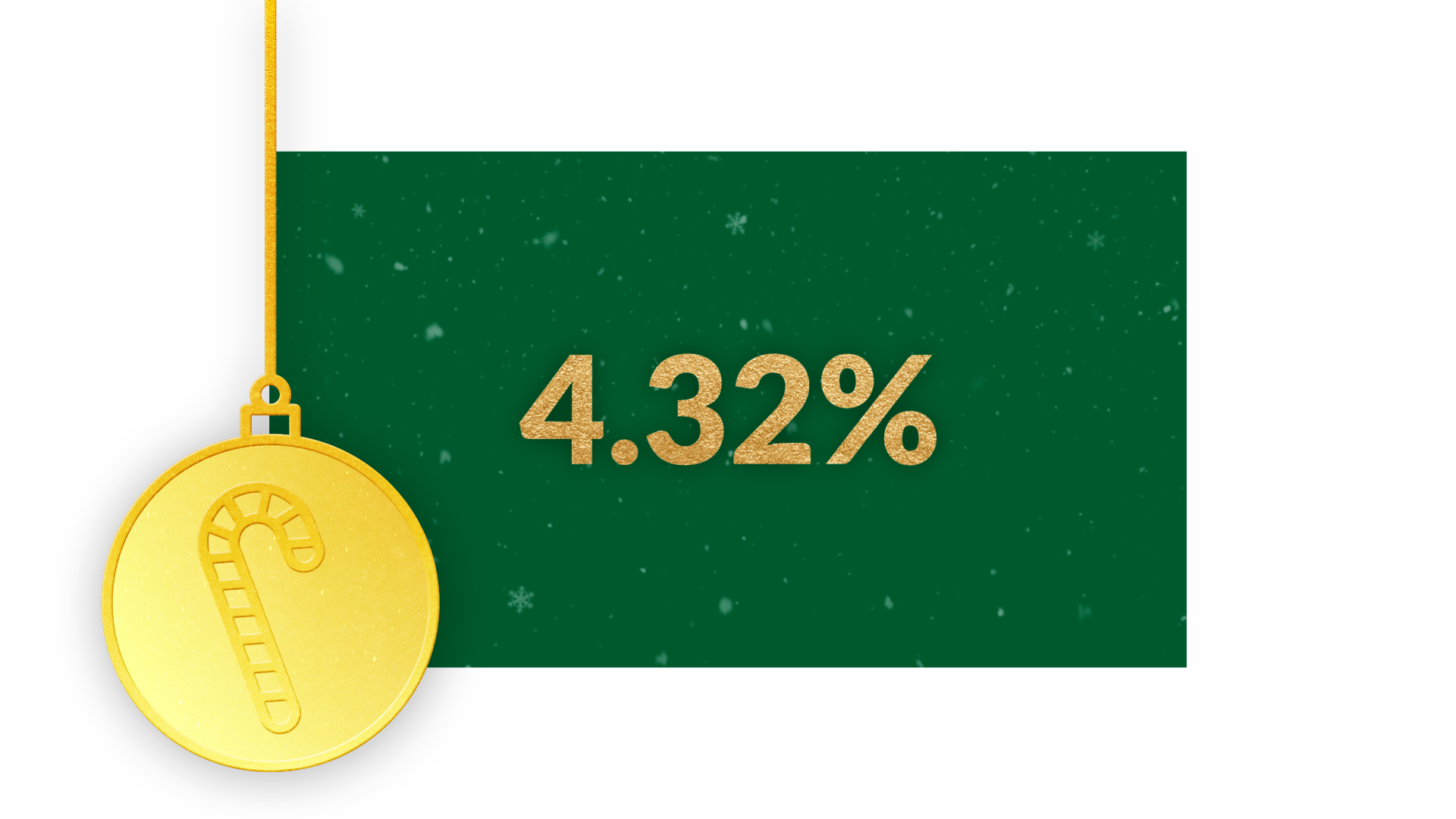

The yield on two-year US Treasuries, which is particularly sensitive to interest rate expectations, dives more than 30bp to close at 4.32% on November 10 - its biggest daily decline since 2008 - after US Consumer Price Index data shows inlation finally came in below forecast for October at 7.7%

With softer inflation data from the Eurozone furher fuelling a broad rally, global government and investment grade corporate bonds bounce to 5% in November, adding a monthly record $2.8tr in market value to a Bloomberg index stretching back to 1990.

Fixed income exchange-traded funds (ETFs) pull in $22.8bn in November, exceeding equities' organic growth for the fifth consecutive month according to Morningstar. After leaking $17bn in the first three quarters of 2022, high-yield bond ETFs come roaring back with $13.3bn of inflows across October and November

After a harrowing year for fixed income investors, 2023 outlooks offer some hope. Bank of America is among several investment banks expecting bonds to bounce back, with its analysts projecting a 13% total return for US investment grade credit along on the back of "lower rates volatility, receding uncertainties and rejuventated credit inflows."